Beware of Your Medicare Premium in Retirement

How Medicare premiums increase in our later retirement years.

Nancy Nawn

6/19/20254 min read

Preparing for retirement requires a projection of expenses that captures the cost of your lifestyle. Paying for Medicare beginning at age 65 is one of the most anticipated costs for retirees. But every client I have ever prepared for retirement was unaware of a term called IRMAA and the substantial impact it can have on Medicare premiums. This additional premium may not show up until a dozen years into retirement, but when it does, you could be paying it for the rest of your life. Read on to learn ways to reduce your risk.

What is IRMAA?

IRMAA is the Social Security Administration’s (SSA) acronym for Income-Related Monthly Adjustment Amount. It is a monthly fee in addition to your regular Part B and Part D premiums if modified adjusted gross income (MAGI) exceeds a certain amount. MAGI is the sum of your adjusted gross income (AGI) on your annual tax return plus any tax-exempt interest, non-taxable Social Security benefits and untaxed foreign income. In other words, some of the income you didn’t pay tax on gets added back for IRMAA determination.

The amount of additional premiums a taxpayer owes, if any, is updated every calendar year for each taxpayer on Medicare. The determination is based on a 2-year lookback of your tax return, so the IRMAA determination for 2025 would look at MAGI for tax filing year 2023. Because incomes can fluctuate in retirement, as the need for cash changes and the requirement to distribute tax-deferred savings increases over time, it is possible to be subject to IRMAA in some years and not in others. It is not a simple expense to plan for many retirees.

Who Pays IRMAA

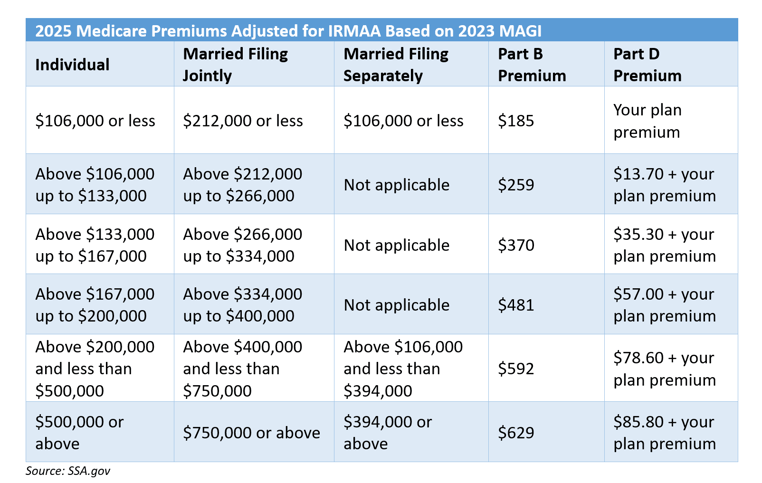

Certain taxpayers, depending upon projected spending, tax-deferred savings and MAGI, will be subject to IRMAA, but first a quick lesson on Medicare. All taxpayers must enroll in Medicare during a 7-month period around their 65th birthday. Recipients are automatically covered by Part A (hospitalization) and most will have coverage for Part B (doctor visits, diagnostics) and Part D (prescriptions). Part A doesn’t have a premium associated with it for most Medicare recipients, only Parts B and D. All Medicare members pay the Part B monthly premium, which is $185, or $2,220 annually, in 2025. The Part D premium is determined by the prescription drug plan of the participant. IRMAA premiums are added to the Part B and Part D premiums based on your MAGI from two years ago. The table below shows what your total premium would be for Part B and Part D with IRMAA in each MAGI bracket.

Looking at this, one may think that her MAGI will likely not fall into the higher ranges. However, when forecasting projected distributions in retirement, I often see clients become subject to IRMAA after their Required Minimum Distributions (RMDs) begin at age 73, especially for single filers. Another component to consider is the sale of assets in retirement, such as a second home or rental property. And if you’re lucky enough to have a pension, this will also be included when determining IRMAA premiums. Pension income is taxable at the federal level and included when calculating MAGI, pushing taxpayers closer to premium increases.

Strategies to Reduce or Avoid IRMAA

By far, the biggest culprit of IRMAA is the Required Minimum Distribution (RMD) in later retirement years. Many savers have taken advantage of tax-deferred retirement savings plans like 401(k), 403(b) and IRA retirement plans. Money saved into these accounts is not included as income on your prior tax returns, but Uncle Sam eventually wants his cut. Distributions we take in retirement are reported on our tax returns and become a part of MAGI. Luckily, planning strategies can help dampen or even eliminate IRMAA premium increases down the road.

For those that have been working for many years and already have much of their savings in a tax-deferred vehicle, Roth conversions could be a way to decrease IRMAA exposure. Roth conversions allow taxpayers to move tax-deferred savings into tax-exempt savings by paying tax at the time of the conversion. Paying the tax and reducing the amount of savings in tax-deferred vehicles will lower future RMDs since the account values will be smaller due to the conversions. And distributions from Roth accounts are not recognized when computing MAGI. Be aware, these transactions are complex and require an analysis of your current tax situation, so always consult with a tax professional such as a CPA or EA before utilizing this strategy.

Another consideration is the number of investments allocated to tax-exempt bonds in retirement. Wealthy taxpayers often utilize tax-exempt bonds to avoid paying tax on income at the federal, state or local levels, but any interest earned on these types of bonds is added back to income when computing MAGI. Strategically managing exposure to tax-exempt bonds could also help reduce the possibility of qualifying for IRMAA.

The Bottom Line

According to the Medicare Board of Trustees, about 6.8 million seniors, or roughly 16.6 percent of all Medicare beneficiaries, will pay approximately $20 billion in IRMAA surcharges in calendar year 2024. The percentage is expected to increase to 25.8 percent by 2031. This is compounded by the increased participation in defined contribution plans that are tax-deferred by nature, thereby driving up RMDs in the future. Younger workers today are more likely to see future IRMAA assessments over their older peers.

If you are subject to IRMAA, assessments can be appealed by filing Form SSA-44 with a local Social Security office. Generally, appeals are only considered for life-changing events including marriage, divorce, the death of a spouse, loss of income, and an employer settlement payment. You may be required to file an amended tax return to have an IRMAA assessment overturned.

Single taxpayers are much more vulnerable to IRMAA, as well as divorcees in retirement since they are assessed at the lowest MAGI level, but many more taxpayers overall will be paying IRMAA premiums in the near future. It is possible to decrease exposure by working with a financial planner and tax professional to develop a diversified tax strategy. The sooner taxpayers plan for the possibility of an IRMAA assessment, the more likely the chance of avoiding it.

WatchDog Planning

Retirement Solutions for Women

text or email

nancy.nawn@watchdogplanning.com

610-364-5838

© 2025. All rights reserved. Disclaimer: Opinions expressed herein are solely those of WatchDog Planning, LLC and are subject to change. Information, resources, and material offered are believed to be from reliable sources, and no representations are made as to their accuracy or completeness. WatchDog Planning, LLC, has no control over the accuracy or content in links enclosed. Fee-only financial planning and investment advisory services are offered by WathDog Planning, LLC, a registered investment advisory firm in the states of New Jersey, Pennsylvania and in other jurisdictions where exempted. Registration does not imply a certain level of skill or training. The information enclosed is not intended as tax, accounting, or legal advice, as an offer or solicitation of an offer to buy or sell, or as an endorsement of any company, security, fund, or other securities or non-securities offering. This information should not be relied upon as the sole factor in an investment making decision. Past performance is no indication of future results. Investment in securities involves significant risk and has the potential for partial or complete loss of funds invested. It should not be assumed that any recommendations made will be profitable or equal any performance noted.